The UK Digital Pound

The UK Digital Pound

Finally A Move Into the 21st Century World of Payments Or Just Too Many Risks?

We live in a legacy world of money. Our transactions are often still based on moving paper money around, and we have basically scaled this into a digital world. At the core of this is the lack of any real cryptographic trust in digitally signing transactions.

For this, the Bank of England is now discussing a CBDC (Central Bank Digital Currency) [2]:

And before you reach for Ethereum smart contracts and ERC tokens, there’s a catch. This is not actually a cryptocurrency, but an electronic payment system. Basically, it will basically be a digital currency, and thus link these coins to a digital wallet which is held by a trusted payment entity (such as a bank or payment provider).

The overall proposed architecture is to use a central bank ledger, which validates transactions. This would not contain any personal data on users and integrate at an API level. Access to this API for users would be through intermediaries — trusted and regulated payment providers. Users would not be able to interact with the core ledger without using an intermediary.

CBDC model

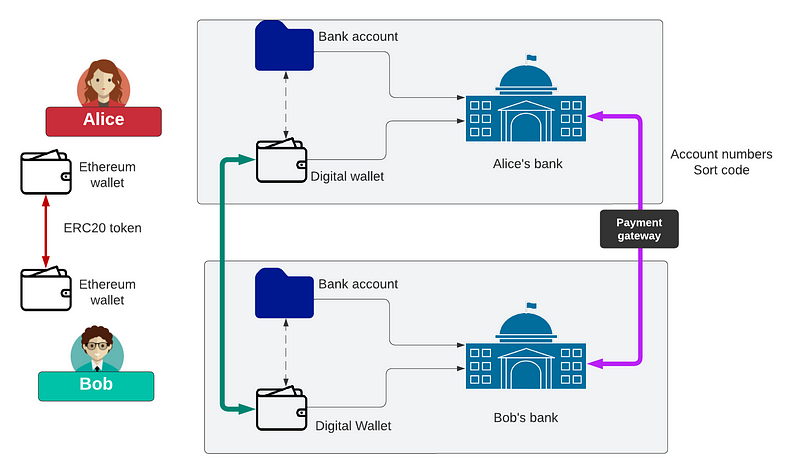

To transfer funds in a traditional way, Alice contacts her bank and enables a transfer to Bob’s bank. The transaction basically involves account numbers and sort codes and is transferred through a trusted payment gateway. This is identified with the purple line in Figure 2.

In the CBDC model, Bob and Alice will own a digital wallet in their bank, and where Alice can move digital tokens from her wallet to Bob’s. Overall, Bob and Alice can move money between their bank account and their digital wallet. The moving of their funds into the digital wallet gives lesser control of funds than the maintenance of bank accounts.

In a traditional cryptocurrency system, Bob and Alice have a public blockchain wallet that contains their private key. In Ethereum, we transfer ERC20 tokens using a digital wallet. This digital wallet contains the private key to sign off the transaction. A smart contract then maintains a table of the owners of each of the ERC20 tokens issued. This relates to the wallet identifier as a hexadecimal address. This is identified as the red line in Figure 3.

The state-of-the-art

There are several existing models for a CBDC, including Project Hamilton, and which is a collaboration between the Federal Reserve Bank of Boston (Boston Fed) and MIT [1]:

The targets are for a minimum of 100,000 transactions

per second and for 99% of all transactions to be completed within five seconds. There should be no loss of funds in the event of a data outage, and privacy is a fundamental part of the design.

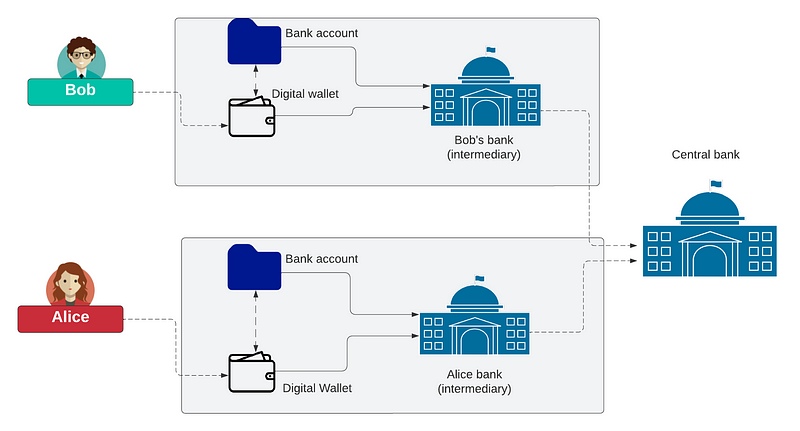

An important element of the design is the use of intermediaries and custody. In terms of trust, we have intermediaries — such as banks, and payment service providers — and which are custodians of the digital wallet. But there is the opportunity for customers to own their own digital wallets — as with an Ethereum wallet. The model can then be “direct” — customer-to-central bank, or “two-tier” — central bank to intermediatory (Figure 4).

The proposed method decouples fund checks with transaction validations. Funds are stored as a 32-byte hash value with an Unspent funds Hash Set (UHS) — Figure 5. The transaction has a similar format to Bitcoin.

Economic concerns

The speed of the transactions and the ease of access to digital currency could enable economic risks

Reduced lending opportunities

As the digital coins are moved to a wallet, they will thus be out of the control of a bank, which means that they could not lend the money to another person — which kinda defeats one of the main functions of a bank. If too much of this money was moved to wallets, it could cause the lending system to stall.

Bank runs

There have been many occurrences of runs on banks, including with Northern Rock. With this, customers queued to get access to the funds, and which generally slowed down the pressures on withdrawals. With a digital pound, this could be made much worse, as customers could withdraw their funds with a simple transfer. Banks could thus risk a run on their funds.

Cybersecurity?

Generally, we trust our banks to look after our money. With a digital wallet, attackers could target hacks, which could have lower levels of control on access to the wallet.

A core part of the Bank of England’s strategy for the digital pound is to develop resilience in both the technical and financial disuptions involved [2]:

Technical challenges

The enablement of a CBDC brings many technical challenges.

Privacy and auditability

There is a significant balance between privacy and auditabilty. The use of zero-knowledge proofs will allow for privacy within transactions, but this will hide the sender and recipient of a transaction. This privacy, though, can restrict auditability and reduce the opportunities for law-enforcement investigations.

Programmability

Most current models must have the full state transition of a transaction to be in-place for a transaction to go ahead (to avoid double spending). Within contract implementations, there may be intermediate states that allow for the digital pound to exist in an intermediate state awaiting an event. For example, Bob might commit to paying Alice for a new car, but she will not accept shipping the car until Bob commits the funds. Once she ships the car, the funds would then stay pending until Bob confirms its receipt. This smart contract associated with the transaction would thus need to store the state of the intermediary state, and not release the funds to Alice until there is a digital proof of receipt from Bob (Figure 6).

Interoperability

A major focus for the digital pound must be the interlinkage with existing Layer-2 payment channel networks. This would also support cross-border transactions but will require integration with other CBDCs in other countries.

Offline payments

In the likely model for the digital pound, there is an interaction between the central bank, and the transacting parties (Bob and Alice). In some circumstances, there could be no Internet connection, and thus there needs to be an offline transaction. This type of transaction will likely require a secret enclave to be setup on a hardware payment device so that the transaction could not be tampered with.

Minting and redemption

It is likely that the CBDC will be responsible for minting and removing the digital tokens. Each of these would be digitally signed by the issuing bank. But, the great risk here is the use of the private key to sign the transactions of the central bank. If an insider in the Bank of England gained access to this, then tokens could be issued or even removed by malicious entities — this is equivalent to printing forged bank notes.

Productionization

While models exist as prototypes, the scale-up to a national level would involve extensive design and implementation skills to make sure there were no ways to compromise the infrastructure.

Denial of service attacks

In a model where Bob and Alice own their private keys, there are no fees for a payment. This means there is no cost to support payment transactions, which means that it could be susceptible to a Denial of Service against the infrastructure — as it will not cost anything to flood the system with valid and invalid transactions. Likely mitigations here are rate-limiting, and the enforcement of a cool-off period before money can be respent on another transaction. Along with this, there could be proof-of-work transactions (such as computing a hash value of a given complexity for each transaction), or fees charged for a given volume of transactions.

Quantum resistance

Existing public key encryption methods — such as ECC and RSA — are at risk against quantum computers. The infrastructure that we create must be resilient to a medium-term attack against transactions. Currently, NIST has defined that Dilithium, FALCON and SPHINCS+ are the preferred solutions for digital signatures, and should replace RSA and ECDSA signatures. For key exchange, Kyber is recommended as a replacement for ECDH. It is likely that any digital currency will support these methods, alongside existing public key methods — but will migrate in time to the post-quantum robust methods.

Conclusions

It is an exciting time. A digital currency will open up new areas of innovation, but one slip-up could bring the whole of the financial infrastructure down in an instant. I repeat again, this is not cryptocurrency, but a trusted digital payment infrastructure. There are good opportunities to improve the detection of fraud and scamming, and truly move to a more trusted financial world.

References

[1] Lovejoy, J., Fields, C., Virza, M., Frederick, T., Urness, D., Karwaski, K., … & Narula, N. (2022). A high performance payment processing system designed for central bank digital currencies. Cryptology ePrint Archive.

[2] The digital pound: Technology Working Paper, Bank of England, 2023.